“In 2019, Spotify bought two podcast networks, Gimlet Media and Parcast. At the same time, it also acquired Anchor, a software platform for creating podcasts. These purchases, which cost the company around $400 million, formed the foundation for its talk-content business. At the time, CEO Daniel Ek called it an “important step” to becoming the leading audio platform…

Four years after those initial strategic plans took off in earnest, Spotify has essentially flipped its priority. On Monday, Sahar Elhabashi, VP of Spotify’s podcast business, publicly posted a memo in which she said the streaming service is moving into the “next chapter” for podcasts on the platform.

Moving forward, Gimlet Media and Parcast will lose their respective branding and join the broader and more generic umbrella of Spotify Studios. Shows will be spun down, and 200 people, largely in podcasting, are losing their jobs.

The new era, Elhabashi noted, will involve “strong discovery and podcast habits for users, thriving monetization and audience growth for creators, and a valuable, high-margin business.” Spotify, which recently launched a TikTok-esque feed, is also encouraging podcasters to put video on the platform.

Translation: very YouTube.”

This is a big pivot.

Spotify spent more than $400 million on Gimlet and Anchor. And hundreds of millions more on exclusive rights to Joe Rogan, Barack & Michelle Obama, Prince Harry & Meghan Markle, and more. (Although the Obamas as well as Prince Harry & Meghan Markle are letting their contracts expire.)

They have over 100 million podcast listeners. And 500 million monthly active listeners overall.

“Spotify has almost 500 million monthly active users — 41% of which are premium subscribers paying a monthly fee for no ads. It generated almost $12 billion in revenue in 2022.

COVID-19 accelerated the streaming trend. The number of podcast listeners jumped 40% globally in the same period, according to EMarketer estimates. Its advertising doubled between 2019-2021 in the U.S. alone, according to PwC.

Analysts project total advertising revenue in the podcasting industry will reach $4.3 billion by 2024.

So what investor wouldn’t be excited about Spotify’s revenue growth and the secular tailwind behind it?

The big issue… Spotify has never made a net profit in its history.

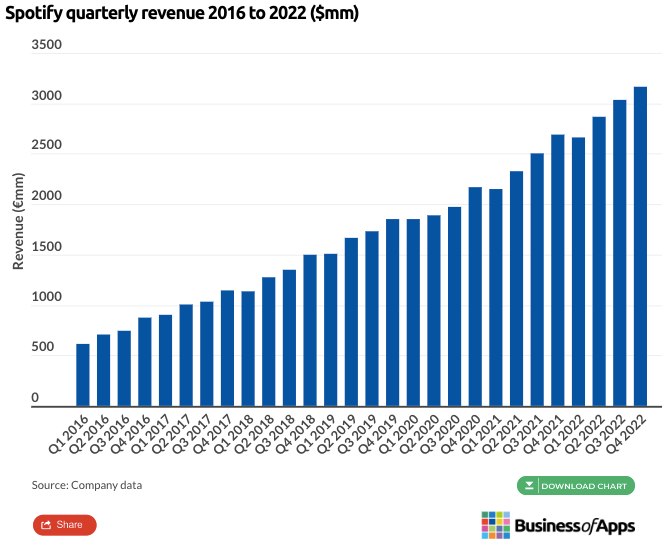

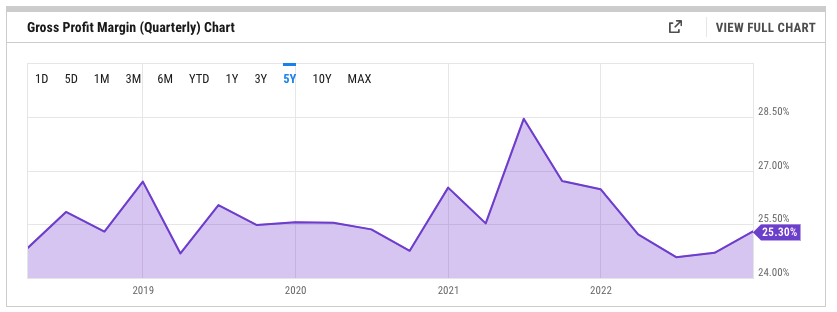

Despite growing quarterly revenues 6x over the past six years… its gross profit margins haven’t budged — ranging in the mid-20s.”

The pivot from Spotify is a step in the right direction. Many companies double down on their business models. It’s good to see Spotify look to their pier — YouTube — as a beacon of profitability.

That’s what makes a good turnaround investment opportunity. Spotify is on our radar now.

However, execution is the hardest part. Let’s see if Spotify will be successful and turn a profit.

2) Calpers Doubling Down On Venture

Most industries are cyclical.

There are booms and busts.

Investing at the troughs is easier said than done. But those who successfully do it stand to make serious money.

Think Warren Buffett buying equities. Sam Zell in real estate. Or Rick Rule in commodities.

However, these are individuals with serious risk appetite.

You’d think public pension funds would shy away from risk. Many of them do. They have mandates and pension obligations.

Pension funds took on uncanny amounts of risk in the zero interest-rate world.

Longtime readers know we’ve written about it over the years.

“Pension systems are supposed to be “safe,” right?

Work for decades. Put money into the respective pension plan. And get promised an expected annual return — usually 7% — after X number of years.

The managers running the pensions are supposed to be good stewards of capital.

There’s an embedded trust between pensioners and the people managing their $35-$40 trillion in assets.

The trust is not to risk too much because it’s people’s retirement money. So most pensions have mandates to invest a large percentage in safe assets (like bonds), and some in stocks. Pension mandates usually follow some sort of traditional 60/40 bond-equity ratio.

But it turns out pension systems levered up and took on as much risk as retail traders due to the global central bank policy of 0% and, of course, negative interest rates.”

Back in October, we wrote about The California Public Employees' Retirement System (CALPERS) — which manages roughly $444 billion — losing $60 billion of their pensioners money due to the drop in public and private equity valuations.

Their performance was so bad, a study concluded CALPERS suffered a “lost decade.”

2021 was the everything bubble. 2022 was the collapse in the everything bubble.

This year though things are back to normal…?! With markets ripping, this is the time for companies to take the gamble and see what investors are willing to pay for their shares.

However, most companies don’t want to go first. They don’t want a false-start. So they wait for others to take the plunge.

We saw how public markets reacted last week when CAVA — a healthy, fast food restaurant chain — went public.

Shares rose almost 100% on its first day trading.

Companies now have the all-clear sign to file for their own public offering.

Some consider Cava’s first day performance as continued fervor in the markets. Others consider it a natural, healthy function of a strong, bull market.

We’re not sure who is right. But expect to see more companies attempt to go public after watching how CAVA’s shares doubled on their first day.

Good investing,

Lance

Thanks for reading Mighty’s Newsletter! Subscribe for free and join our hundreds of readers and clients who receive our weekly missive every Tuesday @ 8:30am EST.

Disclaimer: Mighty Invest LLC (“Mighty”) is an SEC registered investment adviser. Brokerage services are provided to Mighty Clients by Velox Clearing, an SEC registered broker-dealer and member FINRA/SIPC. Clients are encouraged to compare the account statements received from the qualified custodian to the reports provided by Mighty Invest. This should not be considered an offer, solicitation of an offer, or advice to buy or sell securities. Please note that to ensure regulatory compliance and for the protection of our investors and business, we may monitor and read e-mails sent to and from our servers. If you are not an intended recipient or an authorized agent of an intended recipient, you are hereby notified that any dissemination, distribution or copying of the information contained in or transmitted with this e-mail is unauthorized and strictly prohibited. Past performance is no guarantee of future results. The research is based on current public information that Mighty Invest considers reliable, but Mighty Invest does not represent that the research or the report is accurate or complete, and it should not be relied on as such. The views and opinions expressed in this are current as of the date of this email and are subject to change. The information provided is historical and is not a guide to future performance. Investors should be aware that a loss of investment is possible. The securities identified do not represent all of the securities purchased, sold, or recommended for clients. It should not be assumed that investments made in the future will be profitable or will equal the performance of the securities referenced. Additional information, including (i) the calculation methodology; and (ii) a list showing the contribution of each holding to the portfolio’s performance during the time period will be provided upon request. The information transmitted is intended only for the person or entity to which it is addressed and may contain confidential or proprietary material. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information by persons or entities other than the intended recipient is prohibited. If you received this message in error, please contact the sender and delete the material from all computers. The sender does not accept liability for any errors or omissions in the contents of this message which arise as a result of this email transmission