Continuation Funds Squared

“I don’t think this is the norm.” Harold Hope, global head of private market secondaries at Goldman Sachs Group, Inc.

Hope is talking about continuation funds.

We wrote about continuation funds back in June.

Continuation funds are a private equity vehicle to sell off their investments to a new pool of investors. All to get liquidity for their current investors.

The private equity funds then use that fresh capital to raise money for their next fund.

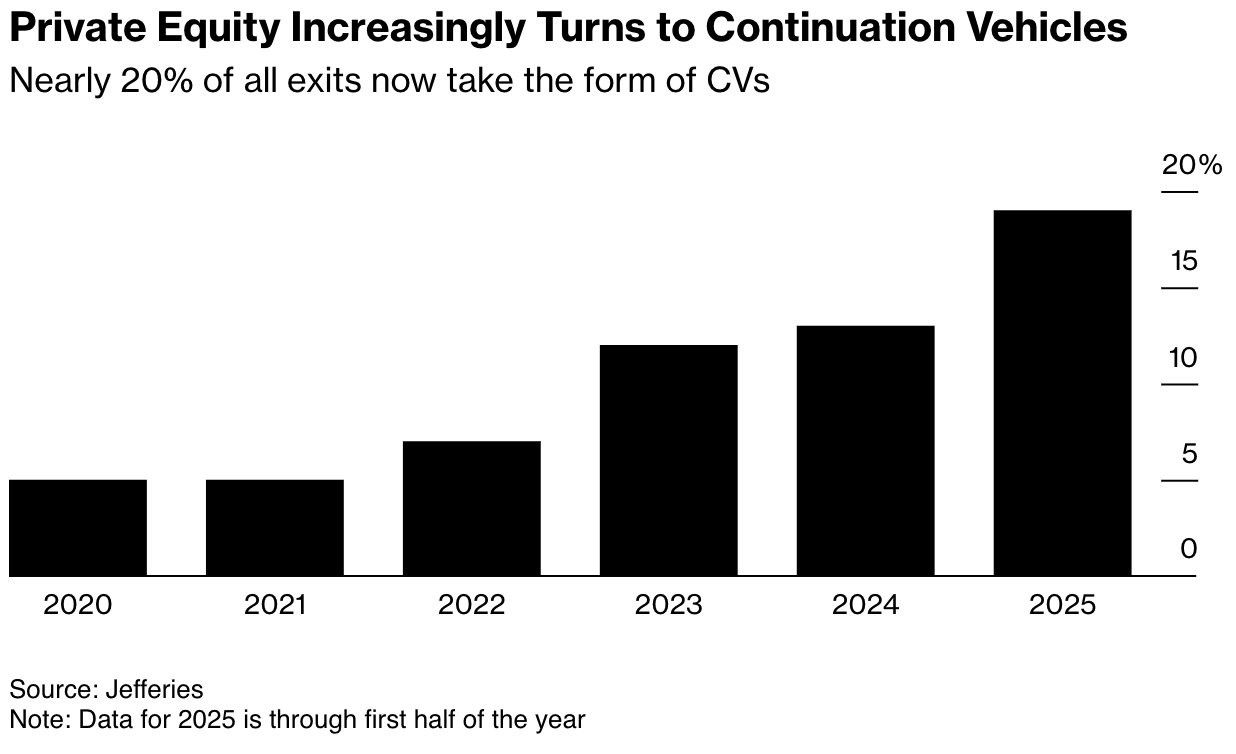

Continuation funds now make up 20% of all private equity exits.

Sound a little fishy? Yeah, it is.

Continuation funds make sense when selling good businesses. But most of these private equity investments aren’t good businesses. Or else they’d take them public or sell them to a larger company.

Private equity funds are just using continuation funds to get liquidity for their next fund.

Longtime readers know this is all part of private equity’s struggle to distribute cash. We’ve written about it several times. (You can read them here and here.)

But wait, there’s more. There’s continuation funds of continuation funds.

From Bloomberg (emphasis added):

“The first time Revelstoke Capital Partners asked investors if it could hold on to Fast Pace Health for longer than usual, they obliged. It was 2020, and a global pandemic had markets on edge.

So Revelstoke put a piece of the medical clinic chain into a new fund and found fresh investors to replace those who wanted their money back. The move allowed some backers to retrieve their cash without forcing the private equity firm to sell at an unattractive price.

Structures like this, often called continuation vehicles, or CVs, have since exploded in popularity as private equity firms limp through a dealmaking drought. Their growth is such that some are now creating CVs of CVs — or CV-squareds, as they’re known…

The stymied deal highlights a tension building between private equity firms and their investors. Buyout shops have a huge backlog of companies to dispose of as elevated interest rates keep a lid on acquisitions. Investors, meanwhile, are growing impatient. And there are no easy solutions.

“I don’t think this is the norm,” Harold Hope, global head of private market secondaries at Goldman Sachs Group Inc., said in an interview. “I can’t think of us having gone into a CV deal where we thought the exit was going to be another CV deal.”

Still, CV-squared deals face unusual amounts of investor scrutiny because sales or public offerings are preferred.

“My preferred exit path in every case is a sale to a strategic buyer who can overpay because they’re going to get the benefit of various synergies,” said Amyn Hassanally, global head of private equity secondaries at Pantheon. “We could get comfortable if the original CV beat the underwriting thesis.”

One problem with CV-squared deals is an inherent conflict of interest between investors and private equity firms, Hassanally said. The process allows private equity firms to renegotiate their fees and interest in the assets as they move them from one continuation fund to another.

Buyout firms should show they have run “a full and fair process” to find accurate prices for their assets even if they’re being rolled into a new continuation vehicle, he said.”

Continuation funds of continuation funds are absurd.

Firms are "selling" companies to themselves twice over. They’re recycling their own portfolios.

PE firms are basically admitting their assets aren't good enough (or the timing isn't right) for a proper sale or IPO, so they kick the can down the road.

Investors prefer "cleaner" exits. Tough luck. CV-squared attracts even more scrutiny because it screams "we couldn't flip this the first time around."

The GP is both buyer and seller in these deals… setting the price themselves with valuations that are likely inflated to justify the move.

Conflicts of interest? Absolutely.

Good investing,

Lance

DISCLAIMER: This is solely our opinion based on our observations and interpretations of events. This should not be construed as personal investment advice.